That’s the central question coming out of the Amazon Q4 2025 earnings call. The numbers were strong. Revenue reached $213.4 billion, operating income hit $25 billion, and AWS accelerated growth to 24% year over year. But the headline isn’t just growth. It’s scale — and the decision to pour roughly $200 billion in capital expenditures into infrastructure, mostly for AI.

This quarter wasn’t about incremental improvement. It positioned Amazon for what Andrew Jassy framed as a generational shift in computing. Investors are now being asked to underwrite an unusually aggressive investment phase. The key issue isn’t whether demand exists today. It’s whether that demand is durable enough to justify the capital intensity being deployed.

Here’s what actually matters.

Table of Contents

Amazon Q4 2025 earnings: The Big Picture

Revenue came in at $213.4 billion, up 12% year over year excluding FX. Operating income reached $25 billion, though that included $2.4 billion in special charges. Trailing twelve-month free cash flow was $11.2 billion. AWS now runs at a $142 billion annualized revenue rate.

These numbers signal operational strength across segments. But they also reflect a company that is increasingly bifurcated:

- AWS driving high-margin, infrastructure-scale growth

- Retail pushing speed, frequency, and everyday essentials

- Advertising compounding at a 22% clip

- AI investments reshaping both internal operations and customer-facing products

Full details are available in Amazon’s Q4 2025 earnings materials on the company’s investor relations site.

The strategic tension is clear: Amazon is funding one of the largest capital cycles in corporate history at a time when AI demand appears almost insatiable. The question is how much of that demand is pull-forward versus structurally permanent.

What the Earnings Show

Taken together, the fourth quarter results do more than confirm momentum. They signal a shift in how Amazon is choosing to deploy capital and accept near-term pressure in exchange for long-duration advantage.

AWS accelerated while margins held despite rising depreciation, suggesting management believes demand durability is strong enough to justify adding capacity ahead of broader enterprise adoption. Retail margins expanded alongside higher fulfillment intensity, indicating that efficiency gains are beginning to absorb rising service expectations. Advertising continued compounding, reinforcing its role as a structurally important, high-margin layer rather than a cyclical add-on.

The common thread across segments is not growth itself, but confidence in utilization. Amazon is signaling that it expects infrastructure, logistics, and engagement investments to remain productively employed rather than underused.

Q3 to Q4: Acceleration Becomes Commitment

The move from Q3 to Q4 2025 marks a clear shift from recovery to conviction.

In Q3, Amazon reported $180.2 billion in revenue with AWS growing 20.2% year over year on a $132 billion annualized run rate. That quarter felt like reacceleration. By Q4, revenue rose to $213.4 billion and AWS growth stepped up again to 24%, lifting the annualized run rate to $142 billion.

The difference is not just seasonal strength. Sequential AWS revenue additions increased, backlog expanded from $200 billion to $244 billion, and management meaningfully raised the scale of its capital plans.

AWS: From Reacceleration to Scale

Q3 projected roughly $125 billion in 2025 CapEx and emphasized adding capacity to meet AI demand. By Q4, the tone shifted toward roughly $200 billion in infrastructure investment, largely centered on AI workloads.

This is a meaningful escalation. Q3 demonstrated that demand was returning. Q4 signaled that management believes demand durability is strong enough to justify accelerating supply.

That bet holds as long as enterprise AI workloads continue moving into production at scale. If AI adoption remains concentrated among a handful of large customers, the larger fixed-cost base becomes more sensitive to utilization swings.

Retail and Advertising: Operating Leverage Emerges

Retail shows a similar sequential pattern. In Q3, North America operating margin was 4.5%, or 6.9% excluding the FTC charge. In Q4, it expanded to 9%. While Q4 benefits from holiday seasonality, the margin expansion reflects cumulative fulfillment efficiencies and regionalization gains.

Advertising followed suit. Q3 delivered $17.7 billion in ad revenue. Q4 reached $21.3 billion, maintaining 22% year-over-year growth while expanding Prime Video ad reach globally.

Across both segments, the theme is operating leverage layered on top of infrastructure investment.

From Q3 to Q4, Amazon did not just grow. It increased its capital intensity while demonstrating improving margin structure. That combination suggests confidence—but it also raises the stakes.

The trajectory works if AWS utilization keeps pace with capacity additions and retail efficiency continues offsetting lower-margin everyday essentials growth. If either softens, the shift from Q3 optimism to Q4 commitment will become more visible in returns.

Earnings Snapshot

- Amazon reported $213.4 billion in Q4 2025 revenue, up 12% year over year excluding FX.

- Operating income reached $25 billion, including $2.4 billion in special charges.

- AWS grew 24% year over year to a $142 billion annualized revenue run rate.

- Trailing twelve-month free cash flow totaled $11.2 billion.

AWS: Accelerating at Scale

AWS revenue grew 24% year over year, the fastest rate in 13 quarters. On a $142 billion annualized base, that growth is not trivial. It represents roughly $7 billion in incremental revenue year over year.

Operating income for AWS reached $12.5 billion in Q4, implying a 35% margin. That’s impressive given the heavy depreciation headwinds from new AI infrastructure.

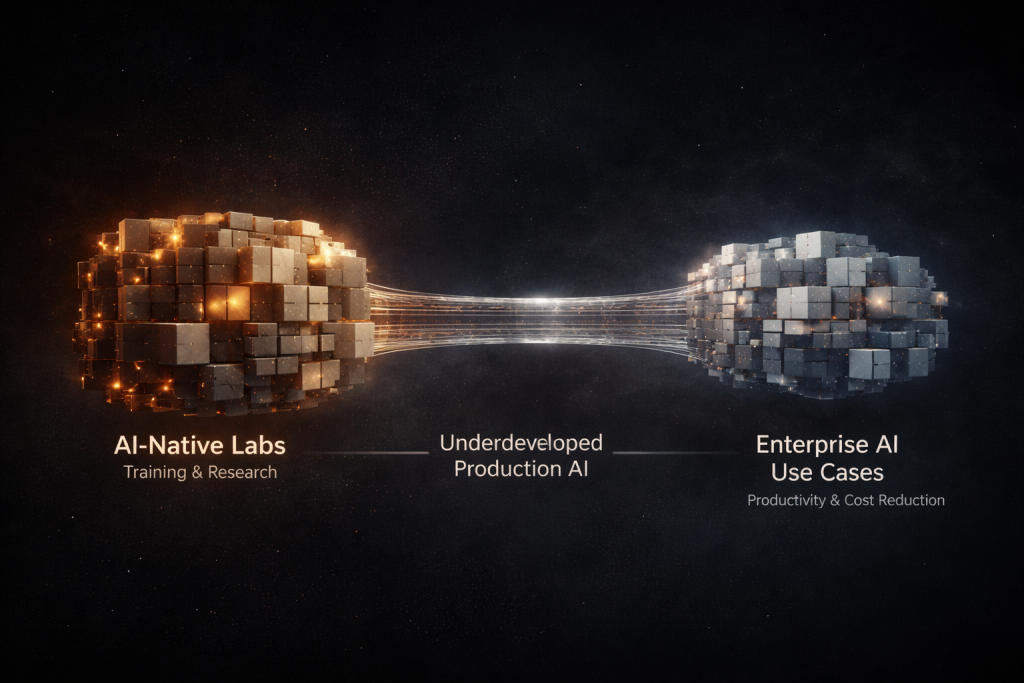

The AI Flywheel

Management described today’s AI market as “barbelled.” On one end sit AI-native labs consuming massive compute for training and research. On the other hand, enterprises deploy AI for cost reduction and productivity. The middle — production AI workloads across industries — remain largely untapped.

That middle is where Amazon sees the long-term prize. Examples of enterprise AI implementations are documented in AWS customer deployments across various industries.

The logic is straightforward:

- AI workloads require data in the cloud

- Enterprises migrating AI also migrate core workloads

- Inference (not training) will drive long-term compute demand

- Lower chip costs unlock broader usage

AWS is positioning itself across the full stack — custom silicon (Graviton, Trainium), Bedrock foundation models, agent frameworks, and infrastructure.

But the strategy depends on several conditions remaining true.

First, inference must indeed become the dominant AI workload over time. Training is capital-heavy but episodic. Inference is ongoing and margin-rich — if utilization stays high. If enterprise AI deployments stall before reaching production scale, utilization rates could soften, pressuring returns on capital.

Second, Amazon’s custom silicon advantage must hold. Trainium and Graviton are framed as 30–40% more price-performant than comparable GPUs or x86 processors. That cost delta underpins both customer demand and AWS margin durability. If competitors narrow that gap, the economics compress.

Andrew Jassy put it plainly:

“As fast as we install this capacity, this AI capacity, we are monetizing it.”

— Andrew Jassy, CEO

That statement is powerful, but it assumes demand will continue to outpace supply. Today, that appears true. By 2027, when power capacity is expected to double again, it must still be true.

Strategic Synthesis of Amazon Q4 2025 Earnings

At this point in the earnings call, several signals are unmistakable.

Amazon’s fourth quarter reflects accelerating AWS growth, expanding retail margins, and sustained advertising momentum. At the same time, the company committed to roughly $200 billion in capital expenditures, largely directed toward AI infrastructure. That combination signals confidence — but it also raises the stakes materially.

This quarter was not about incremental performance. It was about commitment.

AWS growth accelerated to 24% year over year on a $142 billion annualized revenue base, while operating margins held at 35% despite rising depreciation from new infrastructure. Retail continued to improve through higher frequency purchasing, regionalized fulfillment, and logistics efficiency. Advertising compounded quietly, delivering 22% growth and strengthening Amazon’s incremental margin profile.

The fulcrum across all of this is capital discipline.

| Dimension | What Q4 Demonstrated | What Must Hold Going Forward |

|---|---|---|

| AWS demand durability | Growth reaccelerated to 24% with backlog expanding to $244B | Enterprise AI workloads must move from pilots into sustained production usage |

| Capital intensity | Management committed to roughly $200B in infrastructure investment | Utilization rates must keep pace with capacity additions to protect returns |

| Margin resilience | AWS margins held at 35% despite rising depreciation | Custom silicon cost advantages must remain meaningful as competition increases |

| Retail economics | Higher purchase frequency and fulfillment efficiency lifted margins | Productivity gains must offset grocery, same-day, and international expansion costs |

| Advertising leverage | Ad revenue compounded at 22% with expanding Prime Video reach | Amazon must retain direct discovery as AI agents reshape shopping behavior |

The thesis holds as long as three things remain true:

- AI workloads migrate from experimentation into production at scale.

- Custom silicon continues to deliver meaningful price-performance advantages.

- Retail efficiency gains offset the cost of grocery, same-day delivery, and international expansion.

The variable most likely to change the outlook is utilization.

If enterprise AI adoption broadens as management expects, the capital investments underway could generate exceptional long-term returns on invested capital. If adoption slows or remains concentrated among a narrow set of customers, depreciation and fixed costs become visible quickly.

For now, the data supports management’s confidence. AWS backlog expanded to $244 billion. Growth accelerated. Retail engagement deepened. Advertising continued compounding.

The Amazon Q4 2025 earnings call was not about momentum.

It was about conviction.

Investors must now decide whether they share it.

Retail: Frequency Over Flash

While AWS drives valuation narratives, retail remains the economic engine. North America revenue grew 10%. International grew 11% ex-FX. Paid units increased 12% globally.

More important than top-line growth is the shift toward everyday essentials and perishables. One out of three units sold in the U.S. is now an everyday essential. Customers who buy perishables shop twice as often.

Everyday essentials drive habitual engagement. Habit drives lifetime value. That in turn increases ad monetization and Prime retention.

Operational Leverage Comes From Frequency, Not Flash

Amazon also delivered nearly 70% more same-day items in the U.S. year over year. Same-day delivery is now its fastest-growing fulfillment offering. The operational progress is notable. For the third straight year, Amazon improved delivery speed while lowering cost to serve.

That’s not trivial.

The regionalized fulfillment model now spans 10 regions in the U.S. Package consolidation is improving. Robotics exceeded one million units across the network. However, retail margins face their own pressure points.

Amazon plans to open over 100 new Whole Foods locations in the coming years. It’s expanding quick commerce internationally. It’s investing in price competitiveness abroad. These investments support growth — but they also delay margin expansion.

Retail profitability depends on continued productivity gains from robotics and logistics optimization. If those efficiencies plateau while price competition intensifies, margin expansion could stall.

At the moment, North America’s operating margin sits at 9%, up from 8% last year. That’s solid. But sustaining improvement while layering in grocery and quick commerce expansion will require execution discipline.

Advertising: Quietly Compounding

Advertising revenue reached $21.3 billion in Q4, up 22% year over year. Prime Video ads now reach 315 million global viewers, up from 200 million in early 2024.

Advertising is becoming structurally important for two reasons:

- It monetizes retail traffic at a high incremental margin.

- It diversifies revenue beyond pure commerce and infrastructure.

AI plays a role here, too. Amazon introduced AI-driven ad agents to help brands create and optimize campaigns faster.

The risk to watch isn’t demand. It’s funnel compression.

As AI shopping agents — both Amazon’s Rufus and third-party horizontal agents — improve, the path from search to purchase may shorten. Fewer clicks could mean fewer ad impressions.

Jassy addressed this dynamic, arguing that retailer-owned agents have better data and trust. That may be true. But if horizontal AI agents gain consumer traction, the traffic mix could shift.

Advertising resilience depends on Amazon maintaining direct consumer engagement rather than ceding discovery to intermediaries.

For now, engagement metrics look strong. But this is a structural shift worth monitoring over the next few years.

AI in Retail: Rufus and the Future of Discovery

Over 300 million customers used Rufus in 2025. Customers using Rufus are 60% more likely to complete a purchase. That’s meaningful.

AI shopping assistance reduces friction. It increases conversion. It could also reduce search-based browsing.

The upside is clear: higher conversion and stickier ecosystem behavior.

The tradeoff is subtle. If AI compresses the discovery funnel, ad pricing models may evolve. Amazon must balance user experience with monetization.

This is less a near-term earnings issue and more a strategic tension to watch.

Amazon LEO: A Long-Duration Bet

Amazon LEO — its low Earth orbit satellite initiative — remains early. The company has launched 180 satellites and plans 20+ launches in 2026.

LEO introduces near-term operating cost headwinds — roughly $1 billion year-over-year in Q1 North America costs — with commercialization expected later in 2026.

This is a long-duration infrastructure play. It competes in a space with high capital intensity and uncertain pricing power.

The thesis depends on enterprise and government demand for secure, AWS-integrated satellite connectivity.

If LEO successfully integrates with AWS as a private networking extension, it strengthens the cloud ecosystem. If adoption lags, it becomes a capital sink.

At this stage, it’s optionality. But it’s a costly optionality.

Quarter at a Glance

AWS revenue grew 24% year over year with 35% operating margins. Retail North America operating margin reached 9%. Advertising revenue increased 22% to $21.3 billion. Backlog expanded to $244 billion, up 40% year over year.

Key Takeaways

Amazon Q4 2025 earnings mark a transition from reacceleration to full capital commitment. Management signaled that AI-driven cloud demand represents a structural shift, not a temporary spike.

AWS remains the primary growth engine, delivering accelerating revenue growth and durable margins despite rising depreciation tied to infrastructure expansion.

Retail is strengthening through frequency, speed, and operational efficiency, while advertising continues compounding as a high-margin monetization layer. Across all segments, elevated capital spending increases sensitivity to AI utilization rates over the next several years — making execution discipline the defining variable of this cycle.

Future updates will assess whether utilization trends continue to support this investment cycle in Amazon’s Q1 2026 earnings.

What Amazon Is Really Betting On

The Amazon Q4 2025 earnings call ultimately comes down to conviction versus patience.

Management is clearly betting that AI-driven cloud demand represents a structural reset in computing, not a cyclical spike. The scale of capital being deployed reflects that belief. AWS is accelerating, retail efficiency is improving, and advertising continues compounding. On the surface, the pieces fit.

The question investors must answer is not whether Amazon can execute — history suggests it can — but whether utilization keeps pace with ambition. At this scale, small deviations in demand durability matter.

If enterprise AI adoption broadens as expected, this capital cycle could define Amazon’s returns over the next decade. If adoption stalls or concentrates too narrowly, the fixed-cost burden will surface quickly.

This quarter wasn’t about results. It was about commitment. The next few years will determine whether that commitment was well-timed.

For context on how this shift first took shape, see our coverage of Amazon’s Q3 2025 earnings.

Investor Clarifications

Why is capital expenditure rising so sharply?

Amazon plans roughly $200 billion in CapEx, largely for AI infrastructure within AWS. Management believes AI demand durability justifies accelerating capacity buildout ahead of broader enterprise adoption.

Is AWS growth broad-based?

AWS growth accelerated to 24% year over year, with backlog expanding to $244 billion. Management described demand as strong across AI-native labs and enterprise productivity use cases.

How sustainable are AWS margins?

What is driving retail margin expansion?

North America operating margin reached 9%, supported by fulfillment regionalization, robotics deployment, and improved cost-to-serve metrics.

How important is advertising to Amazon’s earnings?

Advertising grew 22% year over year to $21.3 billion. It monetizes retail traffic at high incremental margins and diversifies revenue beyond commerce and infrastructure.

Does AI shopping assistance reduce ad revenue potential?

AI tools like Rufus increase conversion rates but may compress search-based browsing. The long-term impact depends on how consumer discovery behavior evolves.

Get More Earnings Breakdowns and Investor Insights

This site is built for investors who want straightforward, in-depth breakdowns of earnings calls—without the jargon. Whether you follow SoFi, Amazon, Dutch Bros, or other high-growth names, we’ve got you covered. Explore our latest posts and stay tuned—new recaps and insights drop regularly.

Check out our dedicated Amazon page for all the latest posts and deep‑dives, from earnings breakdowns to fresh analyst takes—bookmark it and never miss a beat.

Written by Bryan Smith, creator of Straight From the Call.

I break down earnings calls so you don’t have to. Clear takeaways, no fluff — just the stuff investors care about.

This post is for informational and educational purposes only. It does not constitute financial, investment, or legal advice. Always do your own research or consult a licensed professional before making financial decisions. For the full policy, see our Not Investment Advice & Disclosure Statement